Reloadable prepaid travel cards promise convenience and the certainty of a locked-in exchange rate when spending money overseas. Qantas Pay (formerly Qantas Travel Money) is a popular example – and it earns Qantas Points. But with all these prepaid cards, you often pay a premium in fees and commissions.

An alternative is a bank debit card. These are linked to an ordinary transaction account in Australia and function just like any other debit card you might have. However, some banks offer no international transaction or ATM withdrawal fees, plus no markups on exchange rates. Over one holiday, that could be a lot of money saved without you realising it.

ANZ Rewards Velocity Platinum

- Bonus points

- Up to 80,000 bonus Velocity Points

- Annual fee

- $149 p.a.

- Earn

- Earn 1.5 ANZ Reward Points per $1 spent on eligible purchases up to $2,000 per statement period, then 0.5 Reward Points per $1 you spend on eligible purchases above $2,000 per statement period. Keep on your auto redemption to transfer your ANZ Reward Points to Velocity Points. 2 Rewards Points for 1 Velocity Point.

ANZ Rewards Velocity Platinum

- Bonus Points

- Up to 80,000 bonus Velocity Points

- Annual Fee

- $149 p.a.

- Earn

- Earn 1.5 ANZ Reward Points per $1 spent on eligible purchases up to $2,000 per statement period, then 0.5 Reward Points per $1 you spend on eligible purchases above $2,000 per statement period. Keep on your auto redemption to transfer your ANZ Reward Points to Velocity Points. 2 Rewards Points for 1 Velocity Point.

Get up to 80,000 bonus Velocity Points + $50 back with the ANZ Rewards Platinum Credit Card. Earn 60,000 bonus Velocity Points and $50 back when you spend $3,500 on eligible purchases the first 3 months from approval, plus 20,000 bonus Velocity Points when you keep the card for over 15 months from activation.

Is a prepaid travel card for me? What about Revolut?

Prepaid travel cards, such as Qantas Pay, are best suited to you if:

- You are looking to accrue Qantas Points (specifically for Qantas Pay).

- You’re looking to spend loaded funds predominantly overseas and not overspend.

- Perhaps you might not be eligible for a credit card or want to set up a travel card for a minor.

- You’d like the certainty of knowing what rate you’ve locked in for popular currencies.

The main disadvantage is the price of that convenience: there’s usually some significant padding on the exchange rate.

An exception to this is Revolut, a more innovative version of a travel money card. With Revolut, you can also pre-load currencies or spend ad-hoc using Australian dollars with no international transaction fees. Still, the exchange rate is significantly better than traditional travel money cards.

The main downside is that Revolut limits fee-free ATM withdrawals overseas to A$350 or five per month on the free plan. After this, a 2% or A$1.50 fee per withdrawal applies.

How about a bank debit card?

Not all bank debit accounts are equal. For the best overseas benefits without restrictions, consider:

- UP Everyday: Debit Mastercard

- Bankwest Easy Transaction Account: Platinum Debit Mastercard

- Macquarie Transaction Account: Platinum Debit Mastercard

- HSBC Everyday Global Account: Visa Debit Card

These accounts are entirely fee-free. There are no monthly account-keeping, international transactions, or ATM withdrawal fees. You’ll still be charged any ATM operator fees, which is the norm across all travel cards. Many countries do have some bank operators that don’t pass on fees.

UP, Bankwest and Macquarie use Mastercard, so you can use this online calculator to see what exchange rate you’ll get. HSBC uses internal rates for supported currencies or the Visa rates for non-supported currencies. The advantages of using these debit cards overseas are:

- Significantly improved exchange rate compared to prepaid travel cards.

- Ability to keep your money in a separate savings account to accrue interest and transfer what you need to the transaction account for increased security of funds if your card is lost or stolen.

- No account-keeping or international transaction/ATM fees.

The main disadvantage of UP, Bankwest and Macquarie is you can’t lock in a specific exchange rate if it’s high. What you are charged will depend on the exchange rate of the day. HSBC lets you lock in ten currencies, though their internal rate is usually not as high as the Visa rate.

Comparison of exchange rates

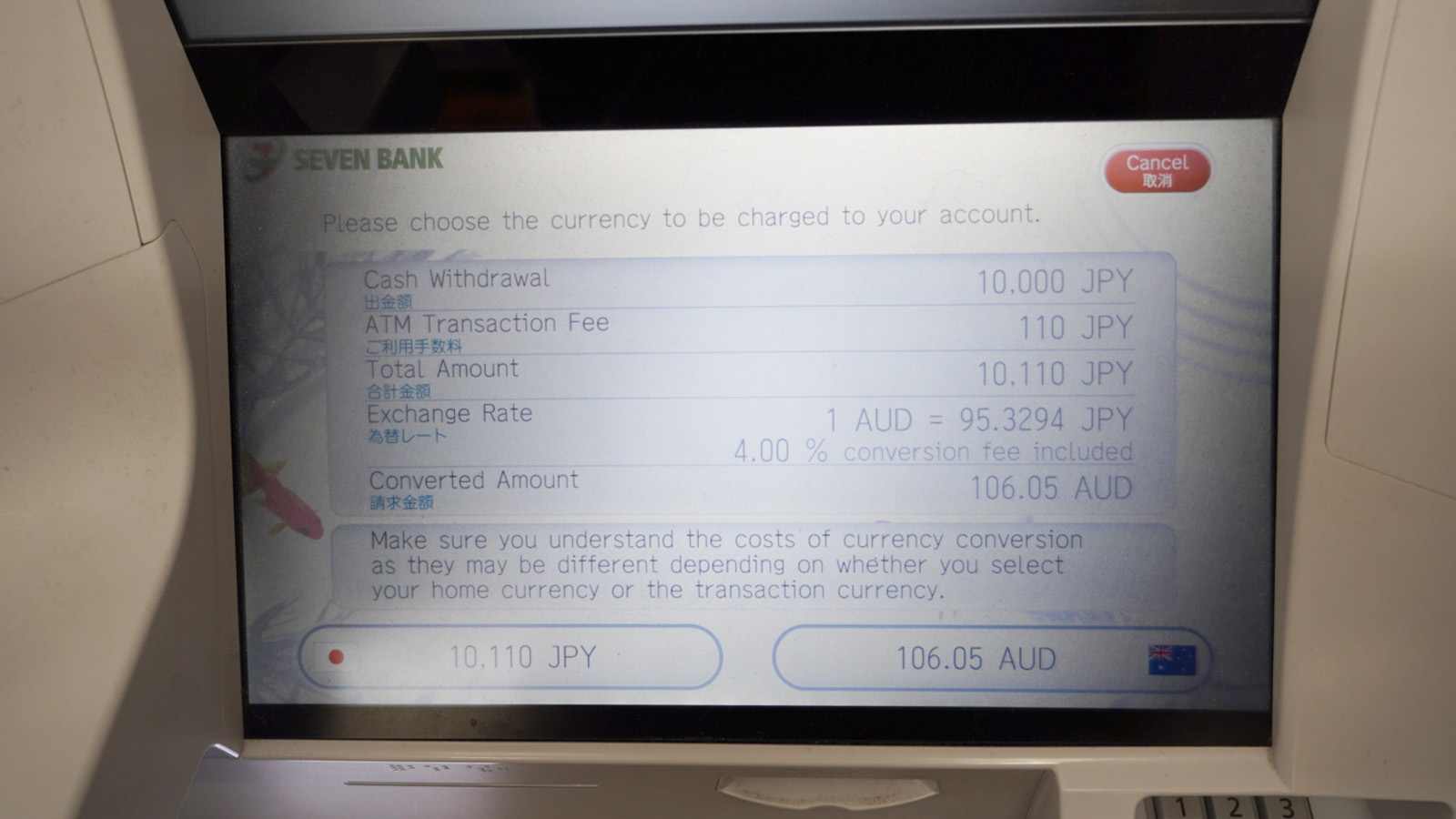

Make sure to look at your card’s exchange rate when converting your AUD into a foreign currency, as this can be the most significant driver of whether you are receiving good value for money.

We’ve compared published exchange rates from a few products below (as of 27 February 2025). The winning currency rate is highlighted in blue, the second place in green, and the lowest rate in red.

| HSBC Everyday Global | UP, Bankwest & Macquarie Transaction | Revolut | Qantas Pay | Travelex Money Card | Commbank Travel Money Card | |

|---|---|---|---|---|---|---|

| US Dollar | 0.617 | 0.6357 | 0.6292 | 0.6014 | 0.6152 | 0.6051 |

| British Pound | 0.4845 | 0.5015 | 0.4967 | 0.4703 | 0.4761 | 0.477 |

| Euro | 0.5856 | 0.6042 | 0.6007 | 0.5711 | 0.5773 | 0.5766 |

| Canadian Dollar | 0.8805 | 0.9088 | 0.9031 | 0.8460 | 0.8672 | 0.8566 |

| New Zealand Dollar | 1.0776 | 1.1099 | 1.1067 | 1.0473 | 1.0631 | 1.0621 |

| Japanese Yen | 91.6582 | 94.78 | 93.8022 | 88.7718 | 89.8944 | 89.87 |

| Singapore Dollar | 0.8218 | 0.8493 | 0.8435 | 0.7893 | 0.8055 | 0.8078 |

| Hong Kong Dollar | 4.77 | 4.9428 | 4.8932 | 4.5861 | 4.6726 | 4.693 |

| Overseas ATM fee (charged by card issuer) | None | None | Free limit of $350-$1,400 per month, then 2% or $1.50 | AUD 1.95; USD 1.95; GBP 1.25; EUR 1.50; NZD 2.50; SGD 2.50; HKD 15.00; CAD 2.00; JPY 160 | None | $3.50 |

Rates were calculated on 27 February 2025 and will fluctuate.

The results above show a clear trend. UP, Bankwest and Macquarie, which all use the Mastercard rate without any mark-up, come out on top. Revolut closely follows behind in second place. Qantas Pay fares the worst in our tests.

What does that mean in real life? Let’s say you want to exchange or spend A$1,500 to use in the USA. At those rates:

- Bankwest/Macquarie: You’ll get US$953.55.

- Revolut: You’ll get US$943.88.

- Qantas Pay: You’ll get US$902.10 + earn 2,250 Qantas Points.

That’s quite a significant spread between the highest and lowest options – about 5.4% less. The difference in exchange rates means you lose out on US$51.45 (~A$82) for the same transaction. Think of it as paying $82 to earn 2,250 Qantas Points – a terrible deal by anyone’s standards.

Summing up

Prepaid travel cards: some people love them, and others hate them. Being a points hacker means knowing when to spot a poor offer and not blindly spending to earn points. With Qantas Pay, you’re paying through the roof with heavily padded exchange rates.

When I travel, I use an Australian debit card with no international transaction or ATM fees to manage my money. I’ll usually withdraw from an ATM (preferably with no operator fee) to get the best possible rate. But even if I can’t dodge the operator fee, the few dollars they charge is still usually a better option than being ripped off by money changers.

Supplementary images courtesy respective frequent flyer programs and financial providers. Point Hacks has no affiliations with the debit card products mentioned in this study.

I would be interested to see how Wise compares in a snapshot comparison between the providers. So far I have found Wise very transparent with their fees and their use of mid-market exchange rates.

I would be interested to see the rate and options differences with the WISE card.These guys also have a system where you can say “if USD goes below 0.59 ,buy 2000aud worth and store it in my USD account “.

Cheers for the article – still a great reference today.

Wondering if you guys will look into comparing it with newer options like Wise’s multi-currency card for example?

Also you should consider Citibank Global Currency account https://www1.citibank.com.au/banking/bank-accounts/global-currency-account. It allows loading foreign currency same as the HSBC Everyday Global account. If you don’t need/want to preload currency, there are a number of transaction accounts with debit cards and 0% FX fee which are usually better than the travel cards in many ways.

Velocity have now closed their Global Wallet

Something that has not been considered is whether the various products have a back up card. Qantas does not. In a recent case a man’s Qantas card was stolen in Paris. Qantas was notified and the card cancelled. Even so, without any pin number the thieves were able to steal 1700 euros, which was eventually returned to the man by Qantas. A new card was promised, but 3 weeks later no card had turned up to the address prearranged. This is not satisfactory at all. The card has still not appeared since the man’s return to Australia. A new card since then has been sent, but this is of

little use now the holday is over. A SECOND BACK UP CARD IS ESSENTIAL.

Hi, I’m really not sure that your assertion is correct about Mastercartd and Visacard rates. Unless you can cite a product that gives these actual rates to consumers without a conversion fee or internationational transaction fee, then your calculations are way off. Pre-paid cards are in fact good value compared to just using and Australian debit or credit card overseas.

Your assertion that “you are forgoing 4-5% of your Australian dollars by using one of these two prepaid travel card compared to the official rates set by the two big card issuers.” is bold. Could you cite a specific card that gives these rates directly? or remove this part of your article? Otherwise … great article and comparison! Thanks.

“Note that this is definitely the absolute best case for both Mastercard and Visa rates. In reality, you will find that no-foreign-exchange-fee cards have a small spread from the above, but they are close enough in practice that the above comparison still holds.”

Generally speaking, using a debit or credit card overseas will result in a more favourable exchange rate than a prepaid travel card. No card will offer the exact official rate that Mastercard or Visa post but the difference is much larger for a prepaid travel card.

Thanks Dan. Love your blog. One thing your readers may also be interested in, is the misconception that you can use these debit cards like a credit card ie when checking into a hotel. For example you haven’t prepaid your hotel booking. The hotel asks to hold funds on your credit card. You hand them your Qantas cash card. The hotel will hold the full amount on a debit card and if you are not careful, they will then on check out charge you the full amount again. The first transaction will take 40 – 60 days to release from a debit card in some countries. So in essence you have been charged double. To avoid this you have to insist the hotel doesn’t create the 2nd transaction and instead uses the first transaction and either increases or decreases the original amount. 8 out of 10 hotels say they can’t do it but a quick chat with the Manager usually sorts this out. Mind you our last visit to Venice ended up being very expensive with a Mexican stand off at reception until we ‘paid’ twice. So the lesson here is these cards are fantastic and useful, in the right circumstances.

My hubbie and I spent two months travelling around the USA in fall last year in a Motorhome. I took an overseas transaction fee free Bankwest credit card, a Velocity global wallet, a Qantas cash card, and a NAB Traveller card. We bank with NAB. We used a card to pay many times a day for fuel, food, tourist entry fees etc. The Qantas card was useless I had preloaded $500 on to both debit cards and it took me many tries to get the money off the qantas card as it would not work at so many places. Also when transferring cash across to it via online banking it took 3 to 5 days to load. The Velocity card was awesome, it worked everywhere from big cities to tiny rural service stations, money transfers via online were instaneous! I withdrew money at many ATM’ s with it, even when the Qantas card wouldn’t work. Also it has a fabulous feature where it emails you your transaction history everyday, and usually very quickly so you know exactly what you have spent and where. Great for checking for fraudulent activity and keeping an eye on your budget. I used the Bankwest card twice just to try it out and it worked fine but with no rewards points and not a very good exchange rate why bother. I also did comparisons for the first week of the exchange rate between Velocity, Qantas, Bankwest and NAB Traveler card and at that time Velocity was slightly better every time. After the first week I didn’t bother anymore as the Velocity card was just so convenient. I used the NAB traveller card once as well, it worked OK, but with no points to be had, again why bother. We spent over $25,000 AU on the trip and I was very happy to see the extra points arrive in my Velocity account. We also flew over and back for free on Velocity points. Premium Economy on the way over and Business Class on the way back, the Star Alliance lounge in LA was fabulous on the return we could eat, have a shower, relax by the outside fire before our long flight home. We have enough Qantas points to do a round the world trip for two with a 5 city stop off, so I will be planning that for our next big trip.

Thanks for sharing your experience and tips!

Hi Dan,

I think there is one feature you didn’t compare, which is how quickly could you load the currency, and make it available to be used. If I am not wrong, at least one of the card you have compared have an instant load feature. (e.g. convert AUD to USD, you could use the USD straight away)

Hi,

thanks for this article.

I have used travel cards in the past and also 28 degrees till I noticed there is a small fee attached to the 28 degrees (it was under AUD$1 last time I looked), which is annoying as it always means you have to add this to your balance if you want to pay the total amount.

So I have swapped to a Citibank debit card (which, I think is the same one as another reader (Geoff) uses). I load it in AUD, use almost any ATM in the world without any fees, and obtain local currency or I can use it as an ordinary debit card in stores. At the end of my trip, any unused money gets returned to my usual bank account. It isn’t attached to any of my usual bank accounts, so much safer to travel with.

I would never return to using any travel cards.

I’ve got wonder about that “inactivity fee”: Is it possible or easy to withdraw from the service later to avoid the fee?

I usually have a big overseas trip every couple of years. This travel card could be useful for me during the trips, but not much use when home. If I just just opt back-out of the service afterward, it’d be a bit more attractive.

I’m sure you can cancel the card. Best to chat to Velocity about that one.

Can I use say the velocity card to do a domestic debit payment and earn points? My biggest gripe is that I can’t use my cards to, say pay someone cash into their bank account, as it’s a cash advance transaction.

I’d say no, that the Velocity Global Wallet card works the same as other cards in this situation.

Of course by locking in your exchange rate you can also win if the Aussie dollar goes down so – that’s a positive 🙂

I’ve been using Qantas Cash for a few years now and while their exchange rates are not the best unless you’ve got a card that has no conversion fee then you’re going to be worse off. The option of a card like 28 Degrees is on the table however by using Qantas Cash I’m earning points which helps to offset any losses.

However there are two very valid reasons that you don’t touch upon:

Who uses cash?

In the past twelve months I’ve had AUD cash in my wallet on 5 occasions (1 Melb Cup Sweeps, 3 for office farewell gifts and 1 for a cash only bar). I’m assuming everyone here puts all spending through their points-earning-credit-cards?

Why would I want $500 cash in my wallet when I’m travelling and at my most vulnerable?

So by using the Qantas Cash debit card for all transactions while OS I’m spending my money, not getting charged ATM Fees or additional conversion fees and the only cash I’m carrying is for tips.

AND I’m earning a high rate of FF Points.

Qantas Cash Bonus Loads.

If you are a regular traveler or online shopper this becomes particularly useful. Regularly throughout the year Qantas offer bonus FF points for loading funds into foreign currencies – $2-4K = 1500 bonus points, $4K+ = 4000 bonus points.

If you’re spending a lot in foreign currencies this adds up nicely – providing even more offset to the mildly lower exchange rate.

I have been using the Citibank – Citi Plus Everyday Account for several years.

https://www.citibank.com.au/aus/banking/everyday_banking/citibank_plus.htm

It is just a bank account so anyone can apply without any hoops to jump through compared to a CC like the 28 degrees. There are no fees for having the account open and no fees for overseas ATM withdrawals. The biggest benefit though is not paying the 3-4% transaction fees on these withdrawals. Obviously no points are earned but the saving of 3-4% far outweighs any gains from points from these travel cards.

I have now complimented this with the new ANZ Rewards Travel Adventures credit card.

https://www.pointhacks.com.au/credit-cards/anz-rewards-travel-adventures-card-guide/

For the $225 annual fee, this card already has some great benefits including a free return flight each year (great for Perth!), 2x virgin lounge passes. It also now earns the equivalent of 0.75 velocity points per dollar (more recently if you transfer during May or November Velocity bonus periods). Finally, this credit card also has no overseas conversion fees. It also has the ability to go into a positive balance for fee free overseas ATM withdrawals.

To sum up, when overseas I use the Citibank Plus account for ATM withdrawals, and the ANZ Rewards Travel for any purchases. I think this is a great combination, and is good to have a backup if you lose either card, knowing you won’t revert to paying exchange fees on your hard earned $$$.

Cheers,

Geoff

Yep, I’ve got a Citi Plus account too!