The Macquarie credit card range offers rewards on everyday spending, no foreign transaction fees, and competitive interest rates by Australian standards. What it doesn’t offer is direct Qantas Points or Velocity Points earn, but it does earn bank points in its own program.

For a general spender, Macquarie cards are genuinely worth considering. For a frequent flyer whose primary goal is to accumulate points toward flights, the picture is more complicated. This review offers an honest account of both sides. You can compare the full range of points-earning credit cards at the Point Hacks credit card guide.

What are the Macquarie credit cards?

Macquarie Bank offers two main consumer credit cards: the Macquarie Black Credit Card and the Macquarie Platinum Credit Card. Both sit in the premium-to-mid-tier bracket of the Australian market and are positioned around low fees, no foreign transaction fees, and a proprietary program called Macquarie Rewards.

Macquarie is best known in Australia as an investment bank and asset manager, but its retail banking arm offers a credit card product that is primarily targeted at its existing home loan customers. The cards offer lower purchase interest rates than most major bank rewards cards, though disciplined points collectors shouldn’t be paying interest on purchases anyway.

Macquarie credit card earn rates and rewards

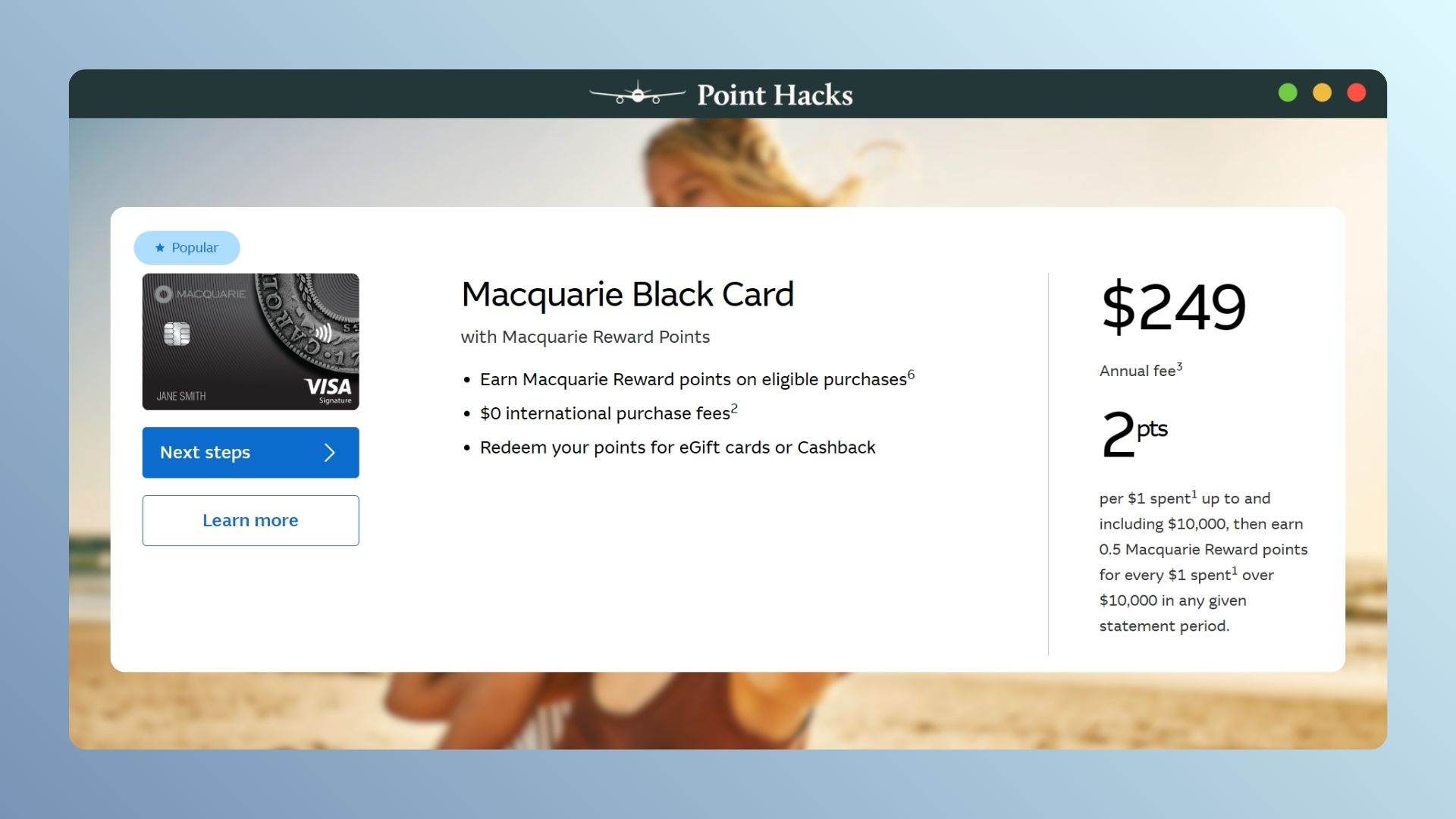

The Macquarie Black Credit Card earns up to 2 Macquarie Rewards points per $1 spent on eligible purchases. The Macquarie Platinum Credit Card earns up to 1 Macquarie Rewards point per $1. Both cards have capped earn rates after $10,000 or $5,000 a month, respectively. If you exceed that cap, you earn half the usual number of points for the rest of the month.

Macquarie Rewards points can be redeemed for cashback and gift cards. Based on Macquarie’s examples, gift cards offer better value for your points than cashback. Here’s an example:

- You can use 21,277 points for a $100 gift card (0.47 cents per point)

- You can use 31,250 points for a $100 cashback (0.32 cents per point)

The key thing to understand about this rewards structure is that Macquarie Rewards points do not transfer to Qantas Frequent Flyer, Velocity Frequent Flyer, or any other airline loyalty program. There are no transfer partners. What you earn stays within the Macquarie ecosystem.

Does the Macquarie credit card earn Qantas or Velocity Points?

No. This is the most important thing for a frequent flyer to know upfront. Macquarie removed airline frequent flyer partnerships from its credit card range some years ago. As of 2026, neither the Macquarie Black nor the Macquarie Platinum Credit Card earns Qantas Points or Velocity Points, directly or through transfer.

This is a significant limitation if building a frequent flyer balance is your primary reason for using a rewards credit card. Across $35,000 of annual spend, a Macquarie Black Card would earn up to 70,000 Macquarie Rewards points, but those points cannot become flight redemptions through Qantas or Virgin Australia.

At best, you could get around $329 worth of gift cards. A comparable card earning Qantas Points directly would produce up to 43,750 Qantas Points on the same spend – enough to fly one-way Business Class or return in Economy between Perth and Sydney (plus fees and taxes). Both options well exceed the value you would get from gift cards at Macquarie.

If you’re a frequent flyer who wants a card specifically to build Qantas or Velocity balances, the Macquarie cards are not the right product. The Point Hacks guide to earning Qantas Points and the Velocity credit card guide cover the alternatives in detail.

Macquarie credit card fees and interest rates

The Macquarie Black Credit Card carries an annual fee of $249. The Macquarie Platinum Credit Card carries an annual fee of $149. Both are typical by premium Australian credit card standards, where annual fees of $250 to $450 are typical for cards with comparable reward earn rates.

The purchase interest rate on Macquarie cards is slightly below the Australian average, which the Reserve Bank of Australia’s January 2025 bank fees bulletin reported as around 20.99% p.a. for standard credit cards. Macquarie’s lower rate is a minor advantage for anyone who occasionally pays interest, though ideally any rewards card balance is cleared in full each month.

There are no foreign transaction fees on either card, which sets them apart from many comparable products in the market. In our eyes, it might be the primary reason you consider taking this card out as a traveller.

Macquarie credit card travel and purchase insurance

The Macquarie Black Credit Card includes complimentary international travel insurance, purchase protection insurance, and extended warranty cover. Insurance is activated by purchasing your return overseas flights with the card before departure, which is a standard activation requirement for most Australian premium travel cards.

The Macquarie Platinum Credit Card includes purchase protection and extended warranty, but does not include international travel insurance. If you want to earn points fee-free while overseas, the Black card might be the better option, as travel insurance is potentially included.

Neither card includes airport lounge access, complimentary lounge passes, or Priority Pass membership. For frequent flyers who value lounge access as part of their travel experience, this is another area where Macquarie falls short compared to cards at a similar or moderately higher annual fee.

Who the Macquarie credit card suits

The Macquarie Black and Platinum cards suit a specific type of cardholder well: a home loan customer who wants a simplified rewards product with no foreign transaction fees, doesn’t carry a balance often but wants a lower interest rate when they do, and is comfortable with a proprietary rewards currency that doesn’t connect to an airline program.

If you travel overseas and want to earn points while avoiding fees, the Macquarie Black Card is a reasonable product for that profile, provided you don’t care about frequent flyer points.

For a genuine frequent flyer whose goal is accumulating enough points for a Business Class flight redemption, the Macquarie cards are better positioned as a ‘nice to have’ secondary card for specific use cases, rather than your main go-to rewards card.

How it compares to other rewards credit cards in Australia

Against comparable-fee cards that do earn Qantas or Velocity Points, the Macquarie’s credit card trades frequent flyer points for the waiving of international transaction fees.

For around the same $249 annual fee as the Macquarie Black, several Qantas and Velocity co-branded cards offer direct points earn at 0.75 to 1 point per $1 alongside complimentary travel insurance. They generally don’t waive international transaction fees, but add lounge access and sign-on bonuses worth far more than the fee difference in year one.

The verdict: should a frequent flyer get the Macquarie credit card?

For most frequent flyers, the answer is no – at least not as a primary card. The absence of Qantas or Velocity Points earn is too significant a limitation for a points-focused strategy.

There are edge cases where it makes sense: as a backup card for everyday or overseas spend, or for a member of your household who doesn’t prioritise frequent flyer points but wants a no-fuss rewards card with low fees and no forex charges. However, at the time of writing, Macquarie Bank is only offering this card to existing home loan customers. There’s no way to apply online.

If you’re evaluating Macquarie because you want a lower annual fee option that still earns some rewards, the ‘no annual fee’ end of the market is worth exploring first. The Point Hacks no annual fee credit card guide covers options that earn Qantas or Velocity Points without a fee. For most frequent flyers, that’s a better starting point than a card that earns neither.

Frequently asked questions

This article is general in nature and does not constitute personal financial advice. Card features and fees are subject to change so always verify current terms directly with Macquarie before applying. Consider your own financial situation before applying for any credit product. Point Hacks may receive a commission from card issuers for applications made through this site.