Credit card travel insurance is one of the most valuable benefits included with premium Australian credit cards. It’s also one of the most commonly misunderstood. While you might save hundreds by not needing a separate policy, it can also leave you completely uninsured if you haven’t met all the conditions.

Research by Mozo found that only 1 in 5 Australians read their full travel insurance policy, even though the specific wording in a Product Disclosure Statement determines whether a claim is paid. For frequent flyers who rely on this cover trip after trip, reading the PDS is a must.

Compare cards with strong travel insurance at the Point Hacks credit card guide.

How complimentary credit card travel insurance works

Complimentary travel insurance provided through a credit card is a group policy. The card issuer has an arrangement with an insurer to cover all eligible cardholders who meet the activation conditions. Because it’s a group policy, the terms are standardised across all cardholders.

You can’t adjust the cover limits, add adventure sports, or extend the trip duration beyond the policy maximum. What you get is what the policy offers to everyone.

This standardisation is both a strength and a limitation. For most trips taken by most frequent flyers, the standard cover is adequate. For trips involving pre-existing medical conditions, extreme sports, or very long durations, it may not be, and a standalone policy purchased separately is worth considering.

The insurer behind most Australian credit card travel insurance policies is typically one of a small number of major underwriters. Multiple card brands often share the same underlying policy structure, which is why the terms can look very similar across products from different banks.

What credit card travel insurance typically covers and what it does not

Most complimentary credit card travel insurance policies in Australia include overseas medical expenses, emergency evacuation and repatriation, trip cancellation for covered reasons, lost or delayed baggage, travel delays, and personal liability cover.

What they typically exclude is equally important. Pre-existing medical conditions are the most significant exclusion in most policies. A condition you were diagnosed with or treated for before the trip will generally not be covered, so you may need to seek specialised cover. Even conditions you consider minor or well-managed can trigger this exclusion.

High-risk activities and adventure sports are commonly excluded, including skiing and snowboarding, scuba diving beyond certain depths, motorcycling, and other activities broadly classified as extreme sports. Some policies include these exclusions even if the activity is commercially operated and considered routine in the destination.

There is also typically a maximum trip duration. Most credit card policies cap cover at between 30 and 90 days, depending on the card. While this covers the vast majority of trips, you might need an alternative if you’re taking extended sabbaticals, working holidays, or multi-leg itineraries spanning several months.

Activation requirements: what you must do before you travel

This is the most practically important section of any card’s travel insurance terms, and the one most frequently overlooked. A common misconception is that simply having the card in your wallet means you’re covered. In most cases, you aren’t!

Most Australian credit card travel insurance policies require you to have purchased at least the return international flight using the card, or the taxes and surcharges on a reward seat booking, for the insurance to activate. If you’re using points, some require the points to come from the card’s rewards program.

Others require a minimum spend on eligible prepaid travel costs such as accommodation or tours. A small number activate automatically regardless of how you paid for your travel, but these are the exception rather than the rule.

If you booked your flights using points and didn’t charge anything to the card, you may not be covered. If your employer paid for the flights and you reimbursed through expenses, you may not be covered. Read the activation conditions in the PDS for your card before every trip, particularly if your booking arrangements deviate from your usual pattern.

Which credit cards offer the strongest complimentary travel insurance in Australia

Not all credit card travel insurance is equal. The areas you should look at are the medical benefit limit, the repatriation benefit, the maximum trip duration, and whether additional cardholders or family members travelling with you are also covered.

The American Express Platinum Card consistently ranks among the strongest for travel insurance. It provides cover for the primary cardholder, spouse or partner, and up to four additional card members on the same trip. There’s no cap on overseas emergency medical expenses. The trip duration limit is 180 days, which is longer than most competitors. Activation is by charging the outbound flight or cruise to the card.

American Express Platinum Card

Offer ends: 25 Aug 2026

- Bonus points

- 200,000 bonus Membership Rewards Points¹

- Annual fee

- $1,450 p.a.

- Earn

- Earn 2.25 Membership Rewards points per $1 on all eligible purchases, except for spend with government bodies, for which you will earn 1 point per $1 spent

American Express Platinum Card

Offer ends: 25 Aug 2026

- Bonus Points

- 200,000 bonus Membership Rewards Points¹

- Annual Fee

- $1,450 p.a.

- Earn

- Earn 2.25 Membership Rewards points per $1 on all eligible purchases, except for spend with government bodies, for which you will earn 1 point per $1 spent

Enjoy 200,000 Bonus Membership Rewards Points when you apply online by 25 August 2026, are approved and spend $5,000 on eligible purchases on your new American Express Platinum Card within the first 3 months.

Mid-tier cards from MyCard, Westpac, ANZ, and NAB sit in the $149 to $370 annual fee range. They typically offer solid international medical cover, 90-day trip duration, and family cover when travelling together. However, specific limits vary so you should always check the current PDS. Several Qantas and Velocity co-branded cards include comparable cover as part of their standard benefits package.

MyCard Premier Credit Card (Velocity)

- Bonus points

- 110,000 bonus Velocity Frequent Flyer Points⁹

- Annual fee

- $300 p.a.

- Earn

- 2 MyCard reward Points per $1 spent on Eligible Transactions online or overseas and 1 MyCard reward Point per $1 spent on Eligible Transactions everywhere else, capped at 200,000 MyCard reward Points over a 12-month period

MyCard Premier Credit Card (Velocity)

- Bonus Points

- 110,000 bonus Velocity Frequent Flyer Points⁹

- Annual Fee

- $300 p.a.

- Earn

- 2 MyCard reward Points per $1 spent on Eligible Transactions online or overseas and 1 MyCard reward Point per $1 spent on Eligible Transactions everywhere else, capped at 200,000 MyCard reward Points over a 12-month period

Earn 110,000 bonus Velocity Points via Autoredemption (converted from 220K MyCard Reward Points) with a MyCard Premier Credit Card when you spend $8,000 on eligible purchases within 90 days from approval.⁹ Automatically transfer myCard Reward Points to Velocity Frequent Flyer Points each month with Autoredemption. Get 0% p.a. for 12 months on balance transfers, a 3% BT fee applies. Balance transfer must be applied for during card application and Balance Transfer rate reverts to Cash Advance rate after the promotional period.¹⁰

Qantas Money Platinum

- Bonus points

- Up to 120,000 bonus Qantas Points*

- Annual fee

- $349 for the first year, $399 p.a.

- Earn

- 1 Qantas Point per whole AU$1 on Domestic Spend up to $10,000 per statement period and 0.5 thereafter. 1.5 Qantas Points per whole AU$1 equivalent on international spend plus 1 additional Qantas Point per whole AU$1 on selected Qantas spend

Qantas Money Platinum

- Bonus Points

- Up to 120,000 bonus Qantas Points*

- Annual Fee

- $349 for the first year, $399 p.a.

- Earn

- 1 Qantas Point per whole AU$1 on Domestic Spend up to $10,000 per statement period and 0.5 thereafter. 1.5 Qantas Points per whole AU$1 equivalent on international spend plus 1 additional Qantas Point per whole AU$1 on selected Qantas spend

Earn 80,000 bonus Qantas Points with the Qantas Money Platinum Credit Card when you spend $5,000 in the first 90 days from card approval, plus 40,000 bonus Qantas Points if you haven’t earned Qantas Points with a credit card in the last 24 months. The card also offers 0% p.a. on balance transfers for 12 months, with a 3% balance transfer fee. Balance transfers must be applied for during the card application and revert to the cash advance rate after 12 months. You’ll also earn 1 Qantas Point per $1 spent and 1.5 Qantas Points per AU$1 spent overseas.

For Velocity cardholders specifically, the Point Hacks Velocity credit card guide notes which cards in that range include travel insurance and what the key terms are.

Cover limits that frequent flyers in particular should pay attention to

Medical cover is the feature of travel insurance that matters the most in an emergency. A medical evacuation from a remote destination, or a major medical event requiring hospitalisation and repatriation from a country with high healthcare costs such as the United States or Japan, can cost hundreds of thousands of dollars.

Policies with uncapped or very high medical benefit limits provide much stronger protection than those with a $5,000 or $10,000 ceiling. Trip cancellation cover is the next most important limit for frequent flyers who book heavily in advance. A policy with a $5,000 cancellation benefit may not fully cover a Business Class international booking that cost $8,000.

Frequent flyers who travel for work should also check whether the policy covers business equipment. Many policies cover personal belongings but have lower sub-limits or outright exclusions for laptops, cameras, or professional equipment.

When credit card travel insurance is not enough on its own

Credit card travel insurance is well-suited to standard leisure and business travel where you are in good health, travelling for a duration within the policy limit, and not engaging in activities outside the policy coverage. In those circumstances, the cover is often equivalent to that provided by a standalone policy.

But it’s not enough if you have a pre-existing medical condition that isn’t covered under the group policy terms. It won’t be suitable when you are travelling for longer than the policy’s maximum duration. It’s useless if you plan to engage in activities that the policy specifically excludes. And you might want better cover if the claim limits are lower than the financial risk you’re carrying on a particular trip.

In those cases, purchasing a standalone policy separately, either in addition to or instead of relying on the card cover, is the appropriate approach. In particular, for pre-existing medical conditions, you might be able to get cover on that standalone policy after completing an online medical assessment.

The two policies can sometimes work together, with the standalone policy picking up what the card policy excludes. But ultimately, you should check the terms of each policy for how they interact.

Tip: common exclusions for motorcyle/moped accidents abroad include not having a licence to drive a motorcycle back home, not wearing a helmet, and/or being under the influence of drugs or alcohol. These are all clearly outlined in the PDS.

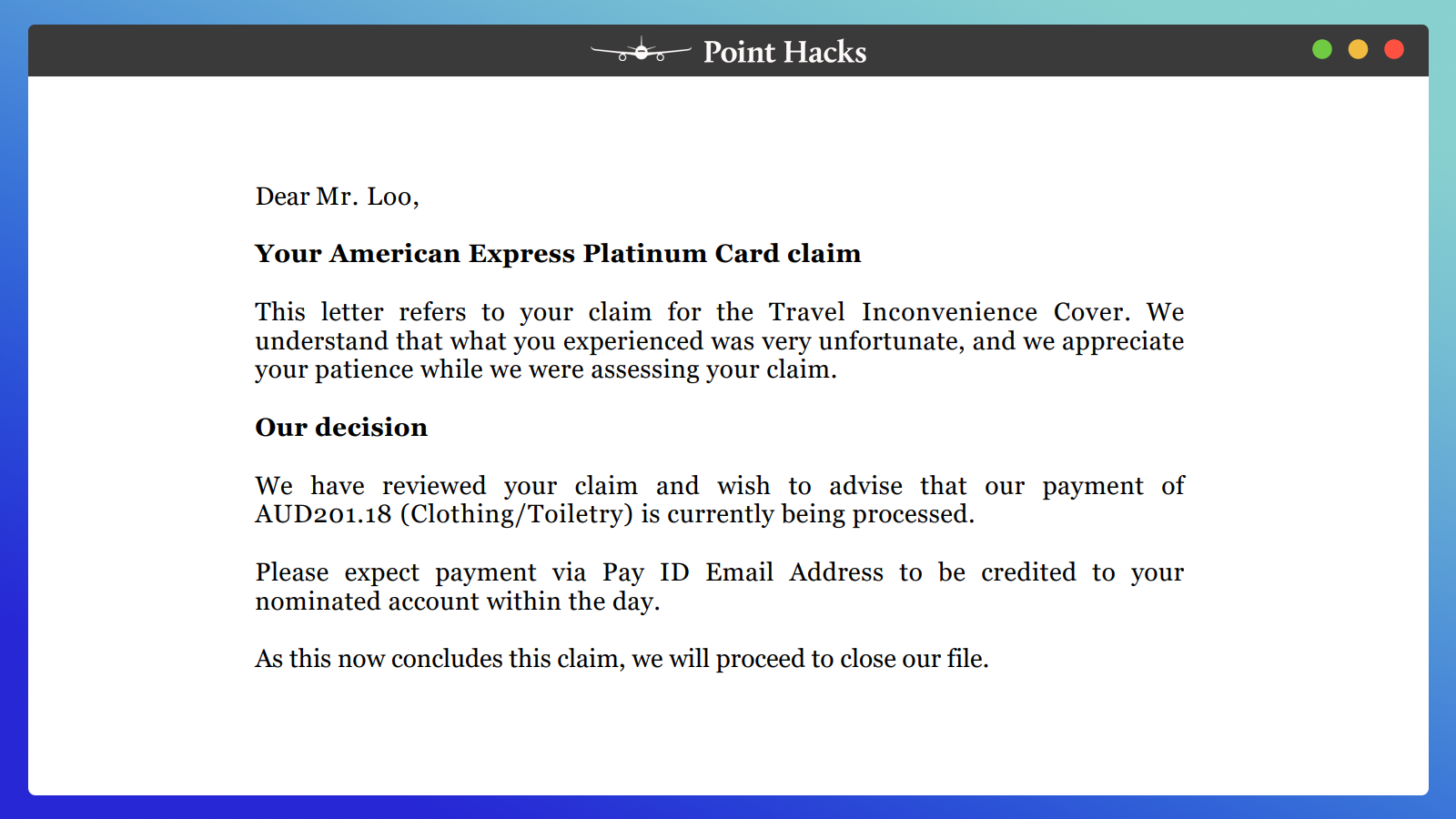

How to make a claim on your credit card travel insurance

Contact the insurer’s emergency assistance line as soon as a medical event occurs while you are travelling. The emergency assistance number is usually printed on the back of the card. Don’t wait until you return to Australia. Calls are often available as a reverse charge.

For non-urgent claims such as travel or baggage delays, you might be able to lodge a claim online if that’s easier. Or you can still phone the insurer to confirm whether your event will be covered.

Keep all receipts, medical reports, police reports where relevant, and any written communication from airlines or hotels confirming delays, cancellations, or losses. A claim without documentation is significantly harder to process. Also keep your boarding passes – printed versions are best.

When you return, gather all supporting documents and submit the claim through the insurer’s claims portal. The insurer is the underwriter, not the bank, so your claim is lodged with the insurance company rather than your card issuer. The card issuer can direct you to the right contact, but is not the decision-maker on claims.

Excess amounts apply to most claims. Check the excess on your specific policy before travel so you understand the minimum loss threshold before a claim becomes financially worthwhile.

Frequently asked questions

This article is general in nature and does not constitute personal financial advice. Travel insurance terms vary by card. Always read the Product Disclosure Statement specific to your card before travelling. Point Hacks may receive a commission from card issuers for applications made through this site.