Every time your business pays a bill, that money could be doing two things at once: settling the expense and accumulating enough points to fly in business class, travel internationally, or reward your team with experiences that a standard bank transfer would never make possible.

For most Australian businesses, it is only doing one. (The first one, if that’s not clear).

Knowing which payment services move money efficiently, which ones convert that spend into points, and how to combine both without overpaying is what separates businesses that build meaningful rewards balances from those that simply pay bills.

Point Hacks has spent years breaking down frequent-flyer programs, transfer partners, and redemption values for every major Australian loyalty program. Whether you are a sole trader trying to earn points on your quarterly BAS, or a growing business paying significant supplier and ATO expenses, this guide will help you understand where the opportunity lies and which platform is most likely to get you there.

What is a B2B payment platform?

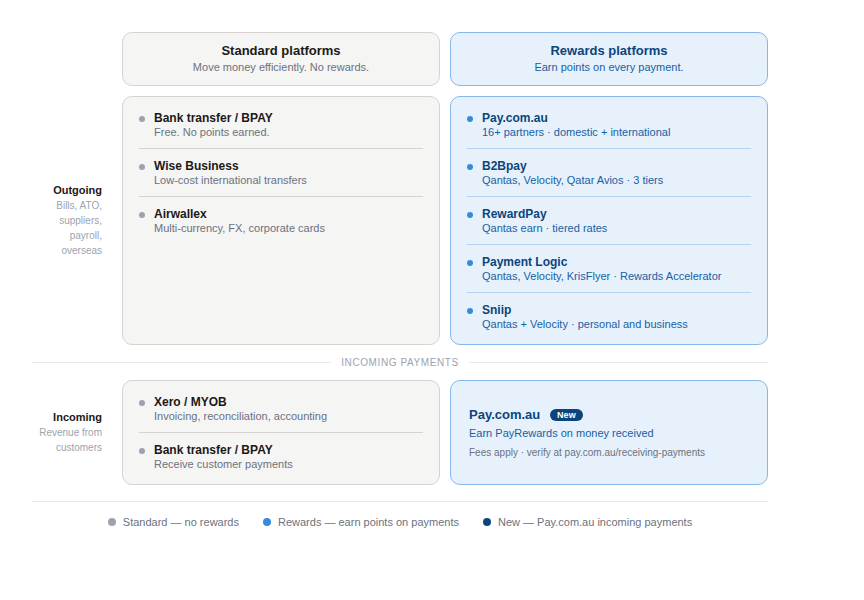

A B2B (business-to-business) payment platform enables your business to send or receive money, whether that is settling a supplier invoice, paying a tax bill, collecting payment from a client, or sending funds overseas. Examples of these include Pay.com.au, Sniip, and Payment Logic.

How Australian businesses turn everyday expenses into points

Not all B2B payment platforms serve the same purpose. The direction of the money determines which type is relevant to you. You could earn points on money going out (common) and money coming in (rare).

Earning points on payments you make

Every dollar leaving your account through a standard bank transfer earns nothing. It settles the bill and disappears. Rewards payment platforms change that entirely, converting expenses you cannot avoid into points that build toward flights, hotel stays, and travel your business makes possible. That opportunity sits almost entirely on the outgoing side.

Earning points on payments you receive

Incoming payments, meaning revenue received from customers, are typically handled by accounting platforms like Xero and MYOB with no rewards component. Our partner, Pay.com.au, has recently launched a feature that lets businesses earn PayRewards points on incoming payments received via PayID or bank transfer, making it the only rewards platform in Australia to cover both directions.

We cover this briefly below, though our focus in this guide remains on outgoing payments, where the broader opportunity sits.

What are the standard payment platforms?

The services most Australian businesses already use don’t earn you reward points. They include:

- Bank transfer and BPAY for free domestic payments

- Xero and MYOB for receiving customer payments and accounting

- Wise Business for occasional low-cost international transfers

- Airwallex for businesses with regular international payment needs.

How do rewards payment platforms work?

Every platform in this category works the same way. You pay the platform by credit card. The platform pays your supplier, the ATO, or any other payee by bank transfer on your behalf. Your credit card treats it as a standard purchase and awards full everyday points on the amount, including on payments like ATO bills, where your card would normally earn nothing or earn at a reduced rate. A processing fee applies.

That is the baseline benefit across every platform below. Where they differ is whether they add their own bonus points on top of your card earnings, which programs those bonus points transfer to, which extra fees apply, and what other features are included.

Paying by bank transfer, rather than by credit card, is also possible on most platforms. You forgo card points but can still earn the platform’s own bonus points where available.

Several platforms operate in this space in Australia. The five most established are covered below. Others, including Lessn, Billr and Blue Chain, also operate in this category with varying fees and earn rates.

How the main rewards platforms compare

All platforms below earn your credit card’s full everyday points as a baseline. The table shows what each platform charges and what it adds on top.

| Pay.com.au | B2Bpay | RewardPay | Payment Logic | Sniip | |

| Cards accepted | Visa, Mastercard, Amex | Visa, Mastercard, Amex | Visa, Mastercard, Amex | Visa, Mastercard, Amex | Visa, Mastercard, Amex |

| Visa / Mastercard fee | 0.80% to 1.20%* | 1.10% to 2.50% | 1.25% | 1.25% | 1.50% personal / 1.36% business |

| Amex fee | 1.75% to 2.10% (tiered by transaction size) | 2.10% to 3.85% | 1.65% to 2.15% (tiered by transaction size) | 1.69% to 2.15% (tiered by transaction size) | 1.29% personal / 1.99%+ business |

| Bonus points on top of the card | Optional -PayRewards at extra cost | Essential: none. Earn Plus: 1 B2B Point per $2. Earn Max: 1 B2B Point per $1. | Optional – Qantas Points at extra cost (0.50% to 3.6%) | Yes – 1 point per $10 standard; up to 10 points per $1 via Rewards Accelerator | Yes – 1 point per $10 (Qantas or Velocity) |

| Bonus points transfer partners | 16+ incl. Qantas, Velocity, KrisFlyer, Asia Miles, Avios, Qatar, Accor, IHG | Qantas, Velocity, Qatar Airways Avios | Qantas only | Qantas, Velocity or KrisFlyer | Qantas, Velocity |

| International payments | Yes, 30 countries | No | No | Yes | No |

| Earn points on incoming payments | Yes – PayRewards on payments received via PayID or bank transfer (fees apply) | No | No | No | No |

| Xero integration | Yes | Yes | No | No | No |

| Subscription options | Free, $85/mo, $165/mo | Free, 3 earn tiers (no monthly fee) | No | No. Lower Visa/Mastercard fees are available through ‘Custom Pricing’, but these forfeit points earn. | No |

All fees exclude GST unless noted and were checked on 15 May 2026. Always verify current rates directly with each provider. * Pay.com.au offers its lowest credit card rates on its $165 per month Premium plan.

Pay.com.au earns your card’s full everyday points on every payment, including payments to the ATO. Its optional PayRewards program adds bonus points on top at an additional fee, transferable to 16+ airline and hotel partners. It is also one of two reward platforms in Australia offering international payments, covering 30 countries. For a full breakdown, see our dedicated Pay.com.au guide.

Note that Pay.com.au is affiliated with Point Hacks.

B2Bpay offers three earn tiers, all free to join with no monthly subscription. Essential earns your card’s full everyday points only at a 1.10% Visa and Mastercard fee. Earn Plus adds 1 B2B Point per $2 spent on top of card points at 2.10%. Earn Max adds 1 B2B Point per $1 spent at 2.50%. B2B Points convert to Qantas or Velocity at 1:1, or Qatar Airways Avios at 2:1. Businesses can choose the tier that best balances fee cost against bonus earn on each payment.

RewardPay accepts Visa, Mastercard, Amex and bank transfer. Its Visa and Mastercard fees are a flat 1.25% plus GST. Amex fees are tiered from 2.15% down to 1.65% depending on transaction size. RewardPay also offers an optional Qantas Points earn program on top of card points, at rates ranging from 0.50% for 1 point per $4 spent up to 3.6% for 2 points per $1, giving businesses control over how many points they earn on each payment.

Payment Logic earns your card’s full everyday points plus its own bonus points. The standard rate is 1 bonus point per $10, but its Rewards Accelerator offers up to 8 tiers, earning up to 10 additional bonus points per $1 at higher fee levels. It also offers international payments. No subscription required.

Sniip earns your card’s full everyday points plus 1 bonus point per $10 paid (Qantas or Velocity). Primarily built for personal bills via an app, with a business tier available. Best suited to sole traders managing personal and business bills together.

What does $100,000 in expenses actually earn?

Every platform earns your card’s full everyday points as a baseline. The table below shows how much a card earning 1 point per $1 on everyday purchases earns across each platform, based on $100,000 in expenses, plus any bonus points the platform adds on top. For point valuations, see our points valuations guide.

| Platform | Max Visa/Mastercard fee | Fee on $100,000 | Card points (1pt/$1) | Bonus points on top | Total points |

| Pay.com.au Free, no PayRewards | 1.20% | $1,200 | 101,200 | None | 101,200 |

| Pay.com.au + PayRewards Tier 1 | 2.20% total | $2,200 | 102,200 | 50,000 Qantas equiv. | 152,200 |

| Pay.com.au + PayRewards Tier 2 | 3.00% total | $3,000 | 103,000 | 100,000 Qantas equiv. | 203,000 |

| B2Bpay Essential | 1.10% | $1,100 | 101,100 | None | 101,100 |

| B2Bpay Earn Plus | 2.10% | $2,100 | 102,100 | 50,000 Qantas or Velocity | 152,100 |

| B2Bpay Earn Max | 2.50% | $2,500 | 102,500 | 100,000 Qantas or Velocity | 202,500 |

| Payment Logic (standard) | 1.25% | $1,250 | 101,250 | ~10,000 | ~111,250 |

| Sniip | 1.50% | $1,500 | 101,500 | ~10,000 | ~111,500 |

| RewardPay | 1.25% | $1,250 | 101,250 | None (unless Qantas tier selected) | 101,250 |

PayRewards points are converted to Qantas Points at a 2:1 transfer rate. B2B Points convert to Qantas or Velocity at 1:1 and to Qatar Airways Avios at 2:1. All fees exclude GST. Figures are illustrative.

At $100,000 in expenses, B2Bpay and pay.com.au generate comparable total points at equivalent tiers, with a negligible gap between them. B2Bpay Essential has the lowest fee in the category at 1.10% with no bonus points on top, while pay.com.au’s free plan sits just above at 1.20% with the same baseline card earn.

Where the platforms diverge is not in how many points you accumulate, but in where those points can take you. B2Bpay transfers to three partners: Qantas, Velocity, and Qatar Airways Avios.

Pay.com.au’s PayRewards transfers to 16+, giving you the flexibility to choose whichever program offers the best availability or value when you want to book. Total points are only part of the story. Here is what those points can actually get you.

Flying business class with your business expenses

The real upgrade in value happens in Business Class, and this is where Pay.com.au’s ability to stack PayRewards on top of card earn, combined with 16+ transfer partners, creates a difference between platforms.

The table below shows how much spend each platform requires to accumulate enough points for a one-way Business Class flight from Melbourne to Singapore on a non-stop reward flight with a full-service carrier.

American Express Business cards are often the highest-earning cards (and most dominant in the Business space), although they come with higher fees. This chart assumes earning 2.25 AMEX points per $1 spent, using the lowest possible processing fee for the expense amount, and transferring points to the most efficient partner.

| Platform | AMEX fee | Points needed | Expenses to earn enough points | Total fees |

| Pay.com.au Free, no PayRewards | 2.1% | 74,000 Velocity | ~$65,777 | ~$1,381 |

| Pay.com.au + PayRewards Tier 1 | 3.1% total | 74,000 Velocity | ~$45,538 | ~$1,411 |

| Pay.com.au + PayRewards Tier 2 | 3.9% total | 74,000 Velocity | ~$34,823 | ~$1,358 |

| B2Bpay Essential | 2.1% | 74,000 Velocity | ~$65,777 | $1,381 |

| B2Bpay Earn Plus | 3.4% | 74,000 Velocity | ~$45,538 | ~$1,548 |

| B2Bpay Earn Max | 3.85% | 74,000 Velocity | ~$34,823 | ~$1,340 |

| Payment Logic | 2.1 – 2.15% | 74,000 Velocity | ~$60,408 | $1,268 |

| Sniip | 1.99% | 74,000 Velocity | ~$60,408 | $1,202 |

| RewardPay | 2.1 – 2.15% | 74,000 Velocity | ~$65,777 | $1,381 |

The cash cost of this flight on Singapore Airlines was $3,202 one-way. Assumes 2.25 Amex points per $1 on eligible purchases, transferring to Virgin Australia Velocity at 2:1. Reward flights are subject to availability. Taxes and carrier charges apply in addition to points redemption. Calculation includes bonus points earned with various providers: PayRewards Tier 1 earns 1 PayRewards point per $1 spent. PayRewards Tier 2 earns 2 PayRewards points per $1 spent. PayRewards transfers to Velocity at a 2:1 ratio. Payment Logic and Sniip both earn Velocity points at 1 point per $10 spent with credit cards.

Across every platform except some B2BPay and Pay.com.au plans, reaching 74,000 Velocity Points requires at least $60,000 in expenses. Those platforms pass through your Amex points but add no meaningful bonus Velocity points.

B2BPay and Pay.com.au changes that. By stacking PayRewards alongside your Amex earn, the total accumulates faster. On Tier 1, you reach the same flight, spending around $45,538, roughly 25% less than every other platform. On Tier 2, that drops to around $34,823, nearly half the spend required elsewhere.

The fees paid across all tiers remain broadly comparable, ranging from $1,202 to $1,411. The difference is not in what you pay, as you save money compared to the cash cost, regardless; it is in how quickly your business expenses get you to a lie-flat Business Class experience. That speed comes from the power of PayRewards.

It also highlights the value of a flexible points currency. Being locked into a single airline program, whether Qantas or Velocity, means your redemption options are dictated by that airline’s availability, pricing, and partner network. When a Qantas seat to your destination is unavailable or priced at a premium in points, you have no alternative.

Pay.com.au’s 16+ transfer partners change that dynamic entirely. With PayRewards, you are not locked into one program. You are building a currency you can direct to whichever airline offers the best seat, availability, or value for your route at the time you want to book. That is the difference between waiting years for an award seat to open up and booking the flight you actually want, when you want it.

Tax reduces the real cost. Platform fees are generally tax-deductible as a business expense, reducing the effective cost by around 30% at the standard company tax rate. GST on fees is also claimable as an input tax credit for GST-registered businesses. Confirm both with your accountant.

International payments: which rewards platforms offer this?

Both Pay.com.au and Payment Logic now offer international payment capability, making them the only two rewards platforms in Australia where you can earn points on overseas transfers.

Pay.com.au covers 30 countries and 11 currencies through its FX partner, SendFX, and earns PayRewards points on every transfer. Point Hacks found its exchange rate was cheaper than CommBank by A$13.69 on a US$650 transfer, including the optional 1.8% PayRewards fee. There are some limitations, such as Visa and Mastercard only (no Amex), no PayID, no recurring payments, and a 2.5-minute rate lock window.

Payment Logic has also launched international payments with reward earnings. Specific country coverage, currencies and fees were not publicly detailed at the time of publication. Verify current terms directly with Payment Logic before using this feature.

For businesses with high-volume or complex international payment needs, a dedicated FX platform like Airwallex remains the stronger operational choice.

Earning points on payments you receive

Pay.com.au recently launched the ability to earn PayRewards points on incoming payments, meaning money received from your customers via PayID or bank transfer. Two earn tiers are available, with points issued the same day as settlement. Funds settle to your account by 2pm each business day. No pay.com.au account is required for your customers to pay you.

This makes Pay.com.au the only rewards platform in Australia that covers both directions of business payments. A full breakdown of how the feature works, its fees, and how it compares to standard payment acceptance tools will be covered in a dedicated article. For current rates and terms, see pay.com.au/receiving-payments.

Note that pay.com.au is affiliated with Point Hacks.

Which platform fits your situation?

The two criteria that most determine which platform suits you are the card you hold and your annual outgoing expense volume. International payments add a third filter.

By card type:

| Card you hold | Best starting point | Why |

| Visa or Mastercard, flexible on program | Pay.com.au | The broadest option in the category: Lowest Visa/Mastercard fee on premium plan of 0.8-1%, 16+ transfer partners, option to stack PayRewards for higher earnings |

| Visa or Mastercard, Qantas or Velocity focused | B2Bpay | 1.10% on Essential tier with card points only, or Earn Plus at 2.10% to also earn B2B Points, converting to Qantas or Velocity at 1:1. No monthly fee on any tier |

| Any card, want to control how many Qantas points you earn per transaction | RewardPay | Flat 1.25% Visa/Mastercard fee with Qantas earn tiers you dial up or down per payment, depending on how many points you want |

| American Express, want to earn across multiple programs | Pay.com.au | Pay.com.au’s own loyalty currency, PayRewards, transfers to 16+ partners, letting Amex cardholders earn in a second program entirely separate from Amex Membership Rewards |

| American Express, Qantas points only at high volume | RewardPay | Amex fee drops to 1.65% at $2M+ in annual payments, making it the cheapest Amex option in the category at scale |

| No rewards card | Pay.com.au or Payment Logic | Without a rewards card, your points earn depends entirely on the platform. Both Pay.com.au and Payment Logic earn bonus points via bank transfer, but Pay.com.au’s PayRewards transfers to 16+ partners, compared with Payment Logic’s two (Qantas and Velocity). When your card isn’t doing any of the heavy lifting, flexible programs are useful. |

By annual expense volume:

| Annual outgoing expenses | Recommended approach |

| Under $30,000 | A rewards credit card alone may be sufficient. At this volume, platform fees can outweigh point value unless redeeming for business or first-class flights |

| $30,000 to $200,000 | Pay.com.au free plan or B2Bpay for baseline card earnings on payments that would otherwise earn nothing. If you anticipate growth beyond $200K, starting with Pay.com.au avoids a platform switch later. |

| $200,000 to $1,000,000 | Pay.com.au Regular plan. The subscription fee starts paying for itself through the lower per-transaction rate |

| Above $1,000,000 | Pay.com.au Premium or enterprise tier. At this volume, even small differences in the fee rate generate meaningful savings, and PayRewards stacking becomes compelling |

If you also pay overseas suppliers:

Pay.com.au is the better-documented option, covering 30 countries and providing published fees and exchange rate data that we have independently reviewed. Payment Logic has also launched international payments with reward earnings, but country coverage and fees should be confirmed directly before use.

Our verdict

Every platform in this comparison earns your card’s full everyday points as a baseline. That alone makes paying through any of them more rewarding than a straight bank transfer on expenses, where your card would otherwise earn nothing.

Beyond the baseline, Pay.com.au leads on program flexibility, with 16+ transfer partners and the ability to stack PayRewards on top of your card earnings. As the business-class modelling shows, stacking advantage compounds at higher expense volumes, reducing how much you need to spend to reach a meaningful redemption, not just how many points you accumulate. For most Australian businesses paying significant supplier, ATO or overseas expenses, it is the strongest long-term choice.

Other platforms suit more specific needs. B2Bpay is the simplest path to Qantas or Velocity bonus points on Earn Plus and above, with no monthly subscription. RewardPay suits Amex cardholders managing large government bills at scale. Payment Logic’s Rewards Accelerator rewards businesses willing to pay a higher per-transaction rate for substantially more bonus points. Sniip suits sole traders managing personal and business bills together.

One important question is: are the points you earn worth more than the fee you pay, and will you use them for a redemption that reflects their real value? For businesses that fly regularly, the modelling in this guide shows the answer is almost always yes, and the platform you choose determines how quickly you get there.

Point Hacks is affiliated with Pay.com.au. All comparisons are made with publicly available data as of May 2026.